Two years ago, Stanger & Company analyzed returns on $11 billion in non-traded REITs (click here for a current list of Non-Traded REITs), which at the time represented about 40% of the market. A WSJ article was christened in order to trumpet the results, but somewhere along the way the Wells REIT public relations people went missing.

The article, unceremoniously entitled Nontraded Real-Estate Trusts Shed Shady Past, Boast Returns, began with the following one sentence paragraph: “Those ugly nontraded real estate investment trusts born out of the limited-partnership industry may finally be looking pretty. But who knows for how long.”

That the public relations people were out on the range is no surprise, as the results of this “analysis” were mixed at best. According to Stanger’s study, internal rates of return averaged 12.5% without dividend reinvestment and 13.6% with dividend reinvestment. Not too shabby, but not so grand either. What about the other 60% of the market? Did Stanger run the numbers and simply decide more red flags than a military base in china that those numbers were unworthy?

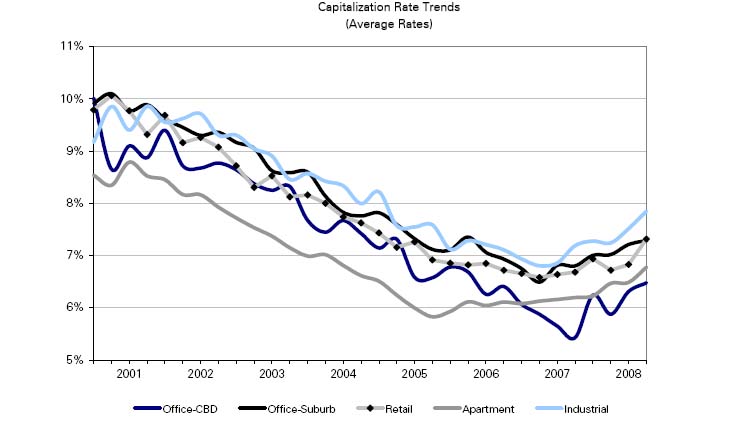

More importantly, how do these reported numbers compare with the rest of the market during that time? As it turns out, it happened to be one of the greatest bull markets in real estate in at least a generation, and had you owned even a dog house in Chihahaua or an igloo in Oaxaca, you would have made heaps of dough:

In 2007, with the torrent of liquidity compressing cap rates to levels not seen in decades, (prices move inversely to cap rates), is a 12.5% IRR really all that impressive? The answer is yuck! not really, and the reason is that the cumulative 15% load (commissions, dealer manager fees, organizational expenses, acquisition fees, asset management fees disposition fees, etc.) stacks the deck in favor of brokers and sponsors, not investors. For an analysis of how some sponsors sometimes play this game of three card monte with shareholders, see What Are Inland Western Shares Really Worth?. Unfortunately, investors often don’t know they’re in trouble until it’s too late , as this article in Kiplingers points out.

FINRA has taken notice, and in a Targeted Examination Letter entitled The Sale and Promotion of Non-Traded REITs issued this month, it seeks to discover just how much.

(Update: for current news and information on Non-Traded REITs, visit The Non-Traded REIT Forum)

The FINRA letter follows in its entirety:

Re: Sale and Promotion of Non-Traded REITs

Targeted Examination Request

March 2009

FINRA’s Enforcement Department is conducting a review of broker-dealer sale and promotion of Non-Traded Real Estate Investment Trusts (REIT). For the purpose of this request a Non-Traded REIT includes: 1) a REIT that is registered with the Securities and Exchange Commission (SEC) but is not listed on an exchange or over the counter market (Non-Exchange Traded REIT); and 2) a REIT that is sold pursuant to an exemption to registration (Private REIT). In connection with this review, and pursuant to FINRA Rule 8210, is requesting the firm provide the following information and documentation.

1. The name of each Non-Traded REIT offered for sale by the Firm;

2. A description of all sales contests, cash and non-cash incentives, as well as other promotions, programs and initiatives that involve, concern or relate to the sale or promotion of Non-Traded REITs. For each item described, indicate to which Non-traded REIT it applied;

3. For each Non-Traded REIT identified in item 1, provide the following information in electronic format:

1. Total number of shares sold to the Firm’s customers;

2. Total dollar amount of shares sold to the Firm’s customers ;

3. Total number of customers purchasing each Non-Traded REIT;

4. Number of customers in the following age groups purchasing each Non-Traded REIT:

1. Under 30

2. 31-54

3. 55-64

4. 65-74

5. 75 and older;

4. Copies of all offering documents for each Non-Traded REIT identified in item 1;

5. For each Non-Traded REIT identified in item 1, provide a registered representative payout schedule or other such document that indicates the commission payout percentage for registered representatives;

6. For each Non-Traded REIT identified in item 1, provide a complete (blank) set of customer application documents;

7. Provide a blank copy of any other customer related documents (not included in your response to item six) used in the sale of Non-Traded REITS, including, but not limited to, customer new account documents, “Accredited Investor” or “Qualified Purchaser” verification forms, risk disclosure documents, checklists, or other documentation concerning REIT yield, liquidity, fees, or per share estimated value;

8. A copy of the portion(s) of the Firm’s written supervisory procedures, compliance manuals or branch manuals that pertain to REITs (Exchange Traded as well as Non-Traded REITs);

9. A copy of the Firm’s suitability guidelines for the sale of Non-Traded REITs, including any guidelines on suggested allocation or maximum percentages for Non-Traded REITs in customer accounts (exclude any information provided in response to item 8). If no responsive documents exist, provide a detailed written description of the guidelines;

10. A list of each type of exception, surveillance or risk monitoring report used by the Firm to monitor activity in Non-Traded REITs. Provide a detailed explanation of the report, including information on the frequency with which the report is run, the type of activity the report is set up to monitor, and the manner in which the data is gathered, interpreted and used by the Firm. In addition, include:

1. Identification of individual(s) responsible for reviewing the report and the names of all individuals receiving copies of the report or a sub-set of the report;

2. Copies of all procedures, explanatory documents or guidelines used in connection with each report;

3. A copy of each type of exception report identified above for the months of June 2008 and December 2008;

4. If no exception or surveillance reports are utilized, provide a detailed explanation of the reviews conducted to monitor the Non-Traded REIT activity at the Firm;

11. Describe the Firm’s risk-based analysis of the Firm’s internal controls and supervisory structure as it relates to REITs;

12. Copies of all customer complaints and arbitration / litigation claims relating to, referring to, or concerning Non-Traded REITS received during the review period. Provide a copy of the Firm’s response;

13. A written description of all internal investigations and/or disciplinary actions related to or concerning REITs or the sale of REITs. Indicate how each matter came to the Firm’s attention;

14. A list in electronic format of customers who purchased Non-Traded REITs during the period January 1, 2008 to the present and have requested to redeem their Non-Traded REIT purchases or who have requested transfers of shares to third parties. The list should include the following fields: (1) customer name (last name, first name, middle initial); (2) name of registered representative (last name, first name, middle initial); (3) registered representative number; (4) date of purchase; (5) date of request; (6) name of Non-Traded REIT for which request was made; (7) number of shares for which redemption or transfer was sought; and (8) whether the redemption or transfer request was honored;

15. Copies of all presentations, marketing materials, advertising and sales literature (as defined in Conduct Rule 2210) that were disseminated outside the Firm, which included information regarding each of the Non-Traded REITs identified in item 1 and Non-Traded REITs in general;

16. Copies of all presentations, marketing materials, written guidance and training materials, including broker-dealer use only material, that were disseminated within the Firm, which included information regarding the Non-Traded REITs identified in item 1 and Non-Traded REITs in general;

17. Provide copies of the 2008 commission run for the Firm’s top 5 REIT producers as measured by total commission.

Click here for a list of non-traded REITs

ShareThis

ShareThis